|

Attribute

|

Details

|

|

Market size Volume in 2024

|

57 thousand tonnes

|

|

Market size Volume in 2035

|

80 thousand tonnes

|

|

Growth Rate

|

CAGR of 3.56% from 2025 to 2035

|

|

Base year

|

2024

|

|

Estimated year

|

2025

|

|

Historical Data

|

2015 – 2023

|

|

Forecast period

|

2026 – 2035

|

|

Quantitative units

|

Demand in thousand tonnes and CAGR from 2025 to 2035

|

|

Report coverage

|

Capacity By Company, Capacity by Location, Production by Company, Demand by End- Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Foreign Trade, Company Share

|

|

Segments covered

|

By End-Use: (Pipe and Fittings, Profiles and Tubes, Films and Sheets, Bottles, Wires and Cables, and Other)

By Sales Channel: (Direct Sale and Indirect Sale)

|

|

Regional scope

|

North America, Europe, Asia Pacific, Middle East and Africa, and South America.

|

|

Pricing and purchase options

|

Avail customized purchase options to meet your exact research needs. Explore purchase options

|

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

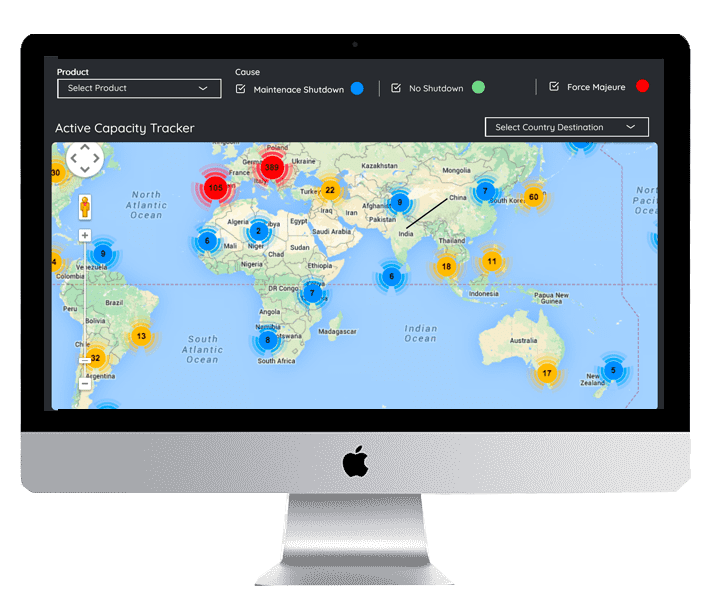

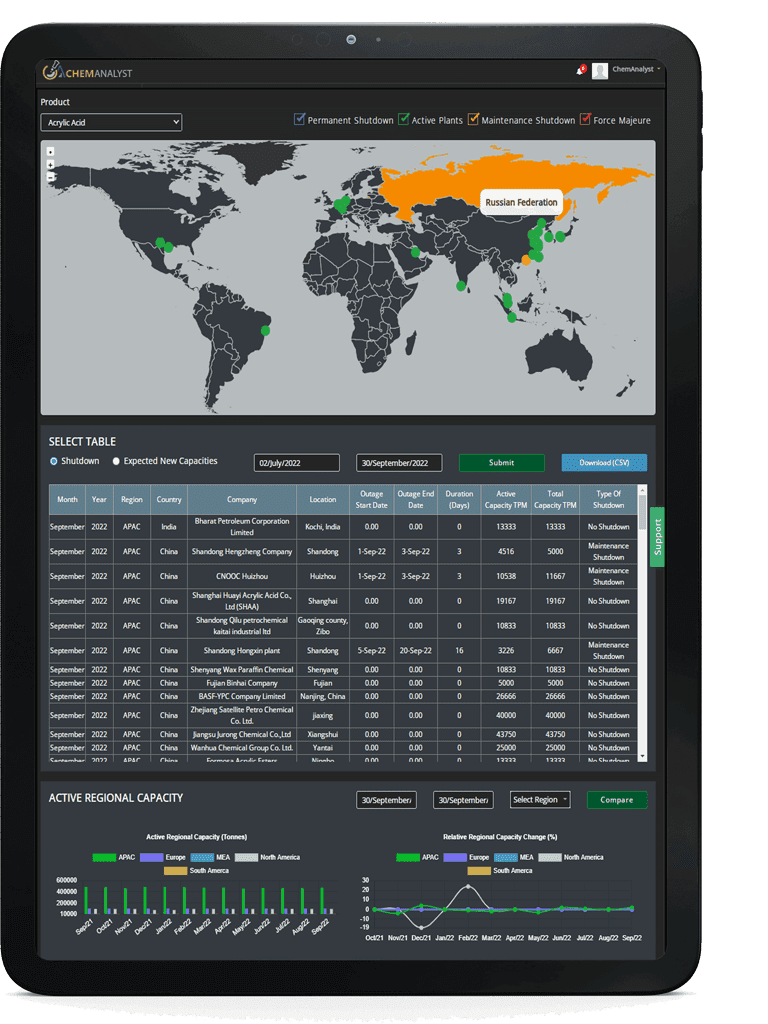

Disruption Tracker reflect the major shutdown on monthly basis which will help you in tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries with a global view of production and consumption capacity loss that reflects the corresponding conversion factors. It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on supply of the product in the market at a Global level.

Q1.

What is the expected global market size of Poly Vinyl Chloride (PVC) in terms of volume for 2035?

Ans:

The global market size of Poly Vinyl Chloride (PVC) is expected to reach approximately 80 million tonnes by 2035, with an expected CAGR of 3.56%.

Q2.

Which end-use industry is dominating the Global Poly Vinyl Chloride (PVC) market?

Ans:

The Pipe and Fittings industry is dominating the Poly Vinyl Chloride (PVC) market with a market share of 44% in 2024.

Q3.

Do you offer single or multiuser license?

Ans:

Online Access 12 Months – Single User License (Up to 3 users can access the database) Online Access 12 Months – Enterprise License (Up to 10 Users can access the database)

Q4.

Will I get access to the analyst who authored this report?

Ans:

You will have 24/7 access to the analyst during the subscription period.

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.