H1 2023: The key players in the global Polycarbonate market in H1 2023 were Covestro, Saudi Basic Industries Corp (SABIC), and Lotte Chemical. However, Covestro was the global Polycarbonate leader in H1 2023. In March 2023, Covestro, a pioneer in Polycarbonate (PC) specialty films, announced about investment of huge sum of double-digit millions of euros for new manufacturing facilities. The investment, which is situated in Thailand's Map Ta Phut Industrial Park, will increase Covestro's capacity and enable it to provide goods primarily used for identification documents, automobile displays, and various electrical and electronic applications. The capacity expansion will be finished in 2025 and create 50 new jobs in the company. In January 2023, Sabic Innovative Plastics had their site shut at Cartagena for a about 30 days for maintenance purposes. The plant restarted its operation in February 2023. In H1 2023, the price of polycarbonate in Asia Pacific region showed a mixed trend. In January 2023, the downstream sectors like electronics & electricals had slow demand for polycarbonate. Polycarbonate market in Japan saw a stockpile of the material. Following a downward trend, the price increased in February 2023 in Asian nations like China and Japan due to increase in number of orders from regional markets. Prices dropped in March 2023 in these Asian nations because there were low number of orders coming in from the international market during the March 2023, indicating the less demand for the polycarbonate. Bearish market sentiment, i.e., decline in price of polycarbonate was observed for the remaining months of H1 2023 in China and Japan.

H1 2022: During H1 2022, Covestro, Saudi Basic Industries Corp (SABIC), and Lotte Chemical were the giant players in the global Polycarbonate market. However, Covestro was the global Polycarbonate leader across the globe which produced approximately 21% of polycarbonate in H1 2022. In H1 2022, Saudi Basic Industries Corporation (SABIC) had revealed about the start of commissioning activities at its polycarbonate manufacturing complex in Tianjin, China. This plant is a joint-venture between Chinese chemical manufacturer, Sinopec and SABIC. It is a 50-50 joint project which has an investment of USD 1.7 billion which was curated by Sinopec Sabic Tianjin Petrochemical Company (SSTPC). Once in operation, it will produce 260 thousand tonnes of Polycarbonate. Regionally, Asia Pacific was the largest consumer of Polycarbonate in H1 2022. In China, polycarbonate prices fluctuated from stable to firm in H1 2022. Prices rose due to strong cost pressure and strong demand from downstream industries across the Chinese industries. In the Indian market, Polycarbonate prices fell in January and February, but in March 2022, the war in Eastern Europe pushed up upstream naphtha prices, impacting polycarbonate production costs across India and other Asian nations. Although, after April 2022, the Polycarbonate prices faced a downward trajectory across Asia. Downstream end-user markets fell sharply during May 2022. A downturn in the upstream raw material bisphenol A market had reduced support for polycarbonate cost across Asia.

H2 2022: During H2 2022, in July and August 2022, Asia Pacific Market sentiment for polycarbonate showed a bearish trend. Although, the exporting costs from countries such as Thailand and South Korea fell. The consumption of Polycarbonate by the downstream industries substantially fell. Fares in the Asian region were fallen supported by the global conflicts. On the supply side, local goods were plentiful and got overstocked. Furthermore, demand by the end-user industries were weak, and market purchase was not so major in July and September 2022 across the Asian nations. A similar trend was observed for the rest of the year. Weak demand from downstream industries had pushed polycarbonate prices down in H2 2022. Weak cost pressure from raw material bisphenol A has supported the downstream derivatives industry, including the polycarbonate market. Downstream industries in China experienced sluggish demand during the end of 2022. During this period, buyers gave fewer orders, which brought material stocks to the market and an abundance of the product. Similar price trend was observed across Europe in the terminal months of 2022. Abundant supplies of natural gas and the cold climate in the European countries contributed to the decline in gas prices. This fall in natural gas prices lowered the cost of producing polycarbonate across Europe, and thus result in the lowered the price of polycarbonate.

The global Polycarbonate market stood at 5200 thousand tonnes in 2022 and is expected to grow at a healthy CAGR of 4.28% during the forecast period until 2032. SABIC, a prominent leader in the chemical industry, has recently entered into an agreement for setting up the world’s first Polycarbonate facility in Cartagena, Spain which will run entirely on renewable power. The plant is expected to turn operational by 2024 and is expected to help SABIC reach it's 2025 clean energy target.

PC, also known as polycarbonate, is a class of thermoplastic polymers having carbonate groups as part of their fundamental chemical component. It has several qualities, such as resistance to moisture, effective heat absorption, and chemical and electrical resistance. Moreover, it improves a substance's thermal and oxidative stability. This substance is frequently utilized to make construction materials, automobile goods, and electronic equipment. Polycarbonate (PC) is a high-performance engineering thermoplastic possessing wide range of characteristics such as outstanding toughness, thermal resistivity and transparency. Manufacturers use Polycarbonate granules, resins or composite materials in a wide range of products such as automobiles, where it finds applications in passenger compartment and vehicle lighting, in buildings and also in electrical and electronic devices such as cords, laptop cases etc. Possessing less than half of the weight of a glass, Polycarbonate is easy to handle, giving designers flexibility to work upon functional and aesthetic designs and introduce innovations in all aspects of automotive lighting.

The primary driver of the Polycarbonate global market is the Electrical & Electronics sector. Due to its high impact and shatter resistance, Polycarbonate finds uses in electronic devices such as cell phones, computers, electrical chargers, gaming boxes, battery covers, and others. Growing demand for more innovative and technologically advanced gadgets is anticipated to further support the market growth in the upcoming years. Furthermore, in the automotive industry, Polycarbonate is used for the production of lightweight exterior and interior parts. Due to its unique properties, PC enable automobile manufacturers to incorporate sleek curves and desirable designs for automobiles while reducing the weight of its components by up to half. The major exterior automotive applications served by polycarbonates and polycarbonate blends include automotive glazing, panoramic roof panels, backlights, and side windows. Rapidly growing consumer demand for stylish automotive designs formulated with component functionality besides maintaining its luxurious appearance would boost the demand for Polycarbonate in the forecast period. Additionally, in the medical sector polycarbonate is used as a replacement for steel and glass for manufacturing instrumentation used in surgery, hemodialysis, drug delivery systems, blood reservoirs, blood filters, etc., that contributes to the polycarbonate market. Owing to these reasons, the Polycarbonate market is estimated to reach nearly 7800 thousand tonnes by the year 2032.

Regionally, the Asia Pacific region is dominating the Polycarbonate market. This region held a market share of approximately 65% in 2022 followed by Europe. Rapidly growing electrical & electronics industry coupled with the increased consumer spending on electronic goods coupled with the multiplying population in developing countries like India, Japan, and China are imposing a higher demand for Polycarbonate for fabricating these goods. Based on production, Asia Pacific region is dominating the Polycarbonate market with China being the key player.

Based on the end-user industry, the global Polycarbonate market is segmented into Electrical & Electronics, Automotive, Construction, and Others. Among these, the Electrical & Electronics sector is dominating the Polycarbonate market. In 2022, this sector held about 60% of the market share and will most likely stay so in the forthcoming years due to production of advanced and innovative electronic gadgets every year.

Major players in the production of Global Polycarbonate are Covestro AG, SABIC, Mitsubishi Engineering-Plastics Corporation, Lotte Chemical Corporation, LG Chem, Formosa Chemicals & Fibre Corp., Teijin Limited, Chi Mei Corporation, Idemitsu Kosan Co. Ltd. (Japan), Zhongsha (Tianjin) Petrochemical, SABIC-Sinopc JV, SHELL-CNOOC, LG Dow polycarbonate, Lutianhua Zhonglan New Materials, Wanhua Chemical, and Others.

Years considered for this report:

Historical Period: 2015- 2022

Base Year: 2022

Estimated Year: 2023

Forecast Period: 2024-2032

This report will be delivered on an online digital platform with one-year subscription and quarterly update.

Objective of the Study:

• To assess the demand-supply scenario of Polycarbonate which covers production, demand and supply of Polycarbonate market in the globe.

• To analyse and forecast the market size of Polycarbonate

• To classify and forecast Global Polycarbonate market based on end-use and regional distribution.

• To examine competitive developments such as expansions, mergers & acquisitions, etc., of Polycarbonate market in the globe.

To extract data for Global Polycarbonate market, primary research surveys were conducted with Polycarbonate manufacturers, suppliers, distributors, wholesalers and Traders. While interviewing, the respondents were also inquired about their competitors. Through this technique, ChemAnalyst was able to include manufacturers that could not be identified due to the limitations of secondary research. Moreover, ChemAnalyst analyzed various segments and projected a positive outlook for Global Polycarbonate market over the coming years.

ChemAnalyst calculated Polycarbonate demand in the globe by analyzing the historical data and demand forecast which was carried out considering the raw materials to produce Polycarbonate. ChemAnalyst sourced these values from industry experts and company representatives and externally validated through analyzing historical sales data of respective manufacturers to arrive at the overall market size. Various secondary sources such as company websites, association reports, annual reports, etc., were also studied by ChemAnalyst.

Key Target Audience:

• Polycarbonate manufacturers and other stakeholders

• Organizations, forums and alliances related to Polycarbonate s distribution

• Government bodies such as regulating authorities and policy makers

• Market research organizations and consulting companies

The study is useful in providing answers to several critical questions that are important for industry stakeholders such as Polycarbonate s manufacturers, customers and policy makers. The study would also help them to target the growing segments over the coming years (next two to five years), thereby aiding the stakeholders in taking investment decisions and facilitating their expansion.

Report Scope:

In this report, Global Polycarbonate s market has been segmented into following categories, in addition to the industry trends which have also been detailed below:

Attribute

Details

Market size Volume in 2022

5200 thousand tonnes

Market size Volume by 2035

7800 thousand tonnes

Growth Rate

CAGR of 4.28% from 2023 to 2032

Base year for estimation

2023

Historical Data

2015 – 2022

Forecast period

2024 – 2032

Quantitative units

Demand in thousand tonnes and CAGR from 2023 to 2032

Report coverage

Industry Market Size, Capacity By Company, Capacity by Location, Operating Efficiency, Production by Company, Demand by End- Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Company Share, Manufacturing Process, Policy and Regulatory Landscape.

Segments covered

By End-Use: (Electrical & Electronics, Automotive, Construction, and Others)

By Sales Channel: (Direct Sale and Indirect Sale)

Regional scope

North America, Europe, Asia Pacific, Middle East and Africa, and South America.

With the given market data, ChemAnalyst offers customizations according to a company’s specific needs.

In case you do not find what, you are looking for, please get in touch with our custom research team at sales@chemanalyst.com

Market Data & Insights

Table of Content

1. Industry Market Size

It is an essential metric for market analysis, as it provides insights into the overall size and growth potential of Polycarbonate market in terms of value and volume.

2. Capacity By Company

On our online platform, you can stay up to date with essential manufacturers and their current and future operation capacity on a practically real-time basis for Polycarbonate.

3. Capacity By Location

To better understand the regional supply of Polycarbonate by analyzing its manufacturers' location-based capacity.

4. Plant Operating Efficiency

To determine what percentage manufacturers are operating their plants or how much capacity is being currently used.

5. Production By Company [Quarterly Update]

Study the historical annual production of Polycarbonate by the leading players and forecast how it will grow in the coming years.

6. Demand by End- Use [Quarterly Update]

Discover which end-user industry (Electrical & Electronics, Automotive, Construction, and Others) are creating a market and the forecast for the growth of the Polycarbonate market.

7. Demand by Region

Analyzing the change in demand of Polycarbonate in different regions, i.e., North America, Europe, Asia Pacific, Middle East and Africa, and South America, that can direct you in mapping the regional demand.

8. Demand by Sales Channel (Direct and Indirect)

Multiple channels are used to sell Polycarbonate. Our sales channel will help in analyzing whether distributors and dealers or direct sales make up most of the industry's sales.

9. Demand-Supply Gap

Determine the supply-demand gap to gain information about the trade surplus or deficiency of Polycarbonate.

10. Company Share

Figure out what proportion of the market share of Polycarbonate is currently held by leading players across the globe.

11. Manufacturing Process

Discover insights into the intricate manufacturing process of Polycarbonate.

12. Policy and Regulatory Landscape

Gain a comprehensive understanding of the policy and regulatory landscape within the Polycarbonate market.

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

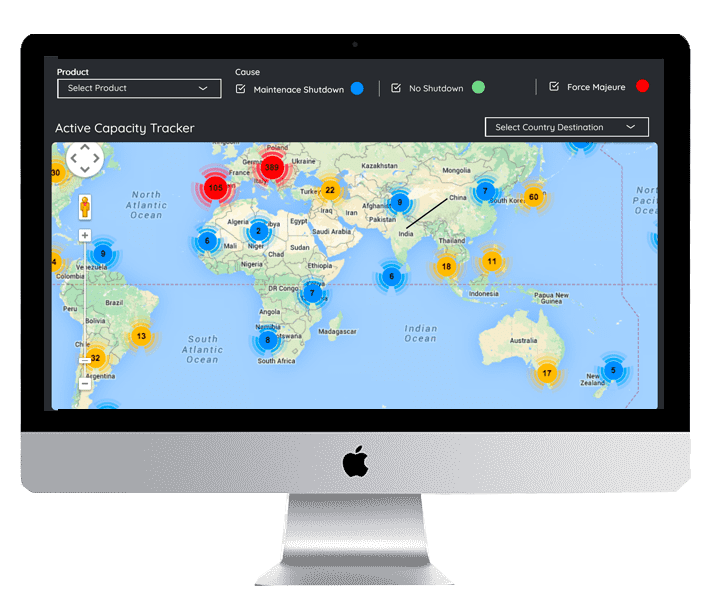

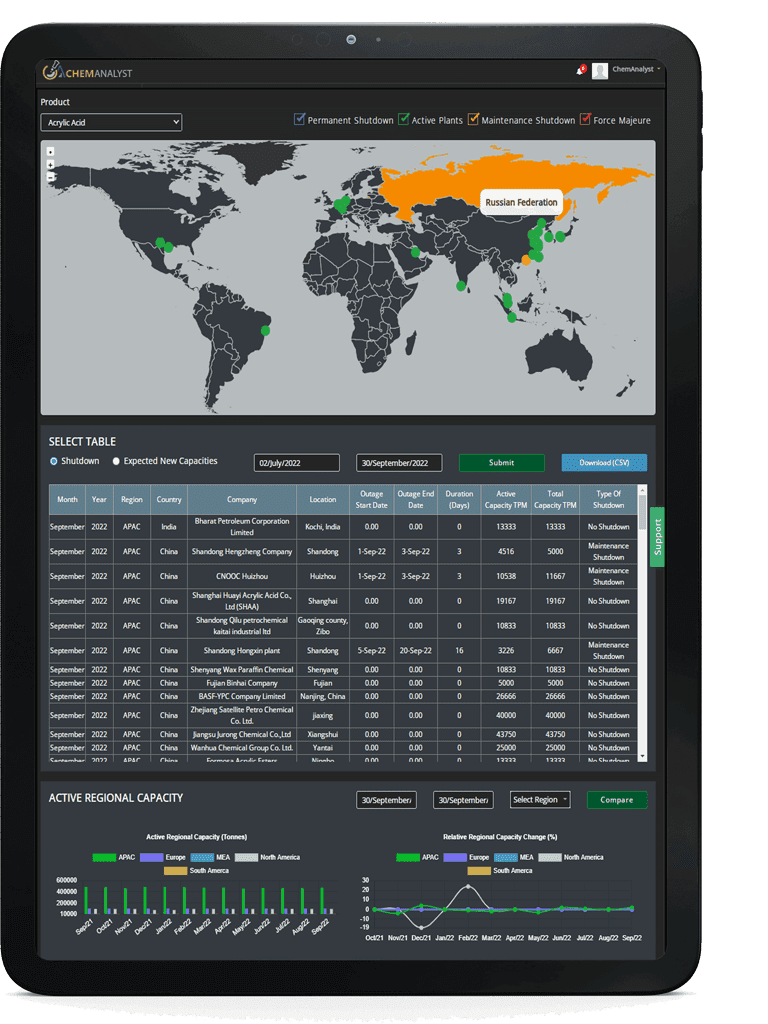

Disruption Tracker

Disruption Tracker reflect the major shutdown on monthly basis which will help you in

tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions

resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries

with a global view of production and consumption capacity loss that reflects the corresponding conversion factors.

It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up

of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case

of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight

into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on

supply of the product in the market at a Global level.

Which region is leading as a consumer of the global Polycarbonate market?

Ans:

Asia Pacific is the largest consumer of the global Polycarbonate market and consumed approximately 65% of the global Polycarbonate market in 2022.

Q2.

Which end-use industry is dominating the Global Polycarbonate market?

Ans:

The Electrical & Electronics industry is dominating the Polycarbonate market with a market share of about 60% in the year 2022.

Q3.

Do you offer single or multiuser license?

Ans:

Online Access 12 Months – Single User License (Up to 3 users can access the database)

Online Access 12 Months – Enterprise License (Up to 10 Users can access the database)

Q4.

Will I get access to the analyst who authored this report?

Ans:

You will have 24/7 access to the analyst during the subscription period.

Our Solutions

Custom Research

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

Techno Economic Feasibility Report (TEFR)

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Price Benchmarking

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.

We use cookies to deliver the best possible experience on our website. To learn more, visit our

Privacy Policy.

By continuing to use this site or by closing this box, you consent to our use of cookies.

More info.