H2 2023: During H2 2023, in the North America region, PVC prices fluctuated. During the third quarter of 2023, Polyvinyl Chloride (PVC) prices in the United States displayed a positive price momentum largely influenced by limited stock availability and high demand. In August 2023, the US PVC market encountered a notable supply shortage attributed to planned shutdowns and maintenance at major PVC plants. This led to a triggered a surge in PVC prices, raising concerns about potential price volatility. Key industry players, including Formosa Plastics, in Texas was closed for maintenance in August and another unit in Louisiana under maintenance in September. Westlake Chemical Corporate also temporarily closed its plant in Louisiana in September, impacted the downstream PVC production. Another major PVC producer, Shintech, scheduled a shutdown of its unit in October 2023 for maintenance. September 2023 saw stable PVC prices due to diminished demand from the construction industry amid weak purchasing enthusiasm in the regional market, aligning with limited inventories. Additionally, the construction sector experienced a decline in demand since August, influencing PVC's prospective market transactions in the third quarter of 2023.

H1 2023: During H1 2023, the top producers of Poly Vinyl Chloride (PVC) in North America were Occidental Petroleum, Georgia Gulf Corp, and Mexichem. In the first half of 2023, the price of Poly Vinyl Chloride (PVC) fluctuated in North America. In the quarter ending March 2023, the price of PVC in the USA experienced a downward trajectory, witnessing a quarterly decline of 3.3%. This decline was attributed to ample inventories and decreased inquiries in the downstream construction sector. Additionally, the USA PVC market faced pressure from rising interest rates and bearish consumer sentiments, impacting the overall PVC offers. Domestic PVC enterprises in the USA encountered competitive cost pressures, influencing the final discussions of the commodity during this quarter. Furthermore, volatility in upstream crude oil prices added input cost pressure to the vinyl monomer value chain by the end of Q1 2023. Moving into the quarter 2 of 2023, PVC prices continued their downward trend, propelled by the persistently sluggish demand in the region's construction sector. Producers faced reduced sales and profits, reflecting the challenging global economic environment and macroeconomic factors impacting commodity performance. Supply chain disruptions and inflationary pressures in the downstream packaging industry characterized the first half of Q2. Despite production challenges faced by major producers like Formosa Plastics Corp. and Westlake Corp., PVC demand remained subdued. The weakened demand was primarily attributed to a slowdown in residential construction in the region due to elevated interest rates by the Fed at the beginning of Q2. In June 2023, the US Department of Homeland Security (DHS) implemented a ban on Chinese imports to the US supply chain as a part of Its Enforcement of the Uyghur Forced Labor Prevention Act (UFLPA).

The North America Poly Vinyl Chloride (PVC) market demand stood at 7.5 million tonnes in 2023 and is expected to grow at a CAGR of 3.8% during the forecast period until 2033.

PVC pipes have been integral in the building and construction sector. Widely utilized for water, waste, and drainage pipeline systems, these pipes resist buildup, scaling, corrosion, and pitting, providing smooth surfaces that reduce energy requirements for pumping. PVC flooring, known for its durability, aesthetic versatility, easy installation, cleanliness, and recyclability, has seen enduring usage. Additionally, PVC is extensively employed in roofing within the building and construction industry due to its low maintenance demands. Polyvinyl Chloride (PVC) stands as a versatile thermoplastic polymer with widespread utility across diverse industries. In the construction sector, PVC is a cornerstone, finding extensive application in pipes, fittings, profiles, and cables due to its commendable durability, corrosion resistance, and cost-effectiveness. Transitioning to the realm of electrical and electronics, PVC is a preferred material for cables, insulation, and wiring, owing to its remarkable electrical insulation properties, prominently used in the production of cable sheathing for power and communication cables. Meanwhile, in the automotive industry, PVC proves indispensable, contributing to the manufacturing of interior and exterior components such as dashboards, door panels, seat coverings, and insulation for wiring harnesses. The medical sector benefits from PVC's biocompatibility and ease of sterilization, incorporating it into applications like tubing, blood bags, and medical devices. Beyond these sectors, PVC extends its influence to consumer goods, playing a role in the production of inflatable structures, vinyl flooring, and various household items. Furthermore, in agriculture, PVC demonstrates resilience, utilized in irrigation pipes, greenhouse coverings, and other agricultural equipment, thanks to its resistance to chemicals and weathering. The diverse applications of PVC underscore its adaptability and contribution to numerous facets of modern life.

In the North American region, the construction industry is poised for moderate growth, propelled by single-family housing, roads, bridges, and institutional construction. According to U.S. Census Bureau, the amount of funds spent in the first 11 months of 2023 on total construction sector was roughly USD 1817 billion. Key growth regions in the United States include Nevada and Texas, particularly in the southern and western areas. Canada anticipates a resurgence in overall construction industry growth, particularly in non-building construction. The United States plays a dominant role in North America's construction industry, with Canada and Mexico also making substantial contributions to sector investments. Thus, North America Poly Vinyl Chloride (PVC) market is likely to reach roughly 11 million tonnes in 2033.

Based on the end-user industry, the North America Poly Vinyl Chloride (PVC) market is segmented into Pipe and Fittings, Profiles and Tubes, Films and Sheets, Bottles, Wires and Cables, and Others. The largest market share of PVC goes with high proportion in Pipes and Fittings about 42% in the year 2023.

Major players in the North America Poly Vinyl Chloride (PVC) market are Amco Polymers, Aurora Plastics LLC, Formosa Plastics Corporation, Ineos, LG Chem, Occidental Petroleum Corporation, Orbia (Mexichem SAB de CV), SABIC, Shin-Etsu Chemical Co. Ltd., Westlake Corporation. and Others.

Years considered for this report:

Historical Period: 2015- 2022

Base Year: 2023

Estimated Year: 2024

Forecast Period: 2025-2033

This report will be delivered on an online digital platform with one-year subscription and quarterly update.

Objective of the Study:

• To assess the demand-supply scenario of Poly Vinyl Chloride (PVC) which covers production, demand and supply of Poly Vinyl Chloride (PVC) market in the globe.

• To analyse and forecast the market size of Poly Vinyl Chloride (PVC)

• To classify and forecast North America Poly Vinyl Chloride (PVC) market based on end-use and regional distribution.

• To examine competitive developments such as expansions, mergers & acquisitions, etc., of Poly Vinyl Chloride (PVC) market in the globe.

To extract data for North America Poly Vinyl Chloride (PVC) market, primary research surveys were conducted with Poly Vinyl Chloride (PVC) manufacturers, suppliers, distributors, wholesalers and Traders. While interviewing, the respondents were also inquired about their competitors. Through this technique, ChemAnalyst was able to include manufacturers that could not be identified due to the limitations of secondary research. Moreover, ChemAnalyst analyzed various segments and projected a positive outlook for North America Poly Vinyl Chloride (PVC) market over the coming years.

ChemAnalyst calculated Poly Vinyl Chloride (PVC) demand across the North America region by analysing the volume of Poly Vinyl Chloride (PVC) consumed by the end-user industries and the forecast is calculated based on the growth rate of end-use industries. ChemAnalyst sourced these values from industry experts and company representatives and externally validated them by analyzing the historical sales data of respective manufacturers to determine the overall market size. Various secondary sources such as company websites, association reports, annual reports, etc., were also studied by ChemAnalyst.

Key Target Audience:

• Poly Vinyl Chloride (PVC) manufacturers and other stakeholders

• Organizations, forums and alliances related to Poly Vinyl Chloride (PVC) distribution

• Government bodies such as regulating authorities and policy makers

• Market research organizations and consulting companies

The study is useful in providing answers to several critical questions that are important for industry stakeholders such as Poly Vinyl Chloride (PVC) manufacturers, customers and policy makers. The study would also help them to target the growing segments over the coming years, thereby aiding the stakeholders in taking investment decisions and facilitating their expansion.

Report Scope:

In this report, North America Poly Vinyl Chloride (PVC) market has been segmented into following categories, in addition to the industry trends which have also been detailed below:

Attribute

Details

Market size Volume in 2023

7.5 million tonnes

Market size Volume by 2033

11 million tonnes

Growth Rate

CAGR of 3.8% from 2024 to 2033

Base year

2023

Estimated Year

2024

Historical Data

2015 – 2022

Forecast period

2025 – 2033

Quantitative units

Demand in million tonnes and CAGR from 2024 to 2033

Report coverage

Industry Market Size, Capacity by Company, Capacity by Location, Operating Efficiency, Production by Company, Demand by End- Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Foreign Trade, Company Share, Manufacturing Process.

Segments covered

By End-Use: (Pipe and Fittings, Profiles and Tubes, Films and Sheets, Bottles, Wires and Cables, and Others)

With the given market data, ChemAnalyst offers customizations according to a company’s specific needs.

In case you do not find what, you are looking for, please get in touch with our custom research team at sales@chemanalyst.com.

Market Data & Insights

Table of Content

1. Industry Market Size

It is an essential metric for market analysis, as it provides insights into the overall size and growth potential of Poly Vinyl Chloride (PVC) market in terms of value and volume.

2. Capacity By Company

On our online platform, you can stay up to date with essential manufacturers and their current and future operation capacity on a practically real-time basis for Poly Vinyl Chloride (PVC).

3. Capacity By Location

To better understand the regional supply of Poly Vinyl Chloride (PVC) by analyzing its manufacturers' location-based capacity.

4. Plant Operating Efficiency

To determine what percentage manufacturers are operating their plants or how much capacity is being currently used.

5. Production By Company [Quarterly Update]

Study the historical annual production of Poly Vinyl Chloride (PVC) by the leading players and forecast how it will grow in the coming years.

6. Demand by End- Use [Quarterly Update]

Discover which end-user industry (Pipe and Fittings, Profiles and Tubes, Films and Sheets, Bottles, Wires and Cables, and Others) are creating a market and the forecast for the growth of the Poly Vinyl Chloride (PVC) market.

7. Demand by Region

Analyzing the change in demand of Poly Vinyl Chloride (PVC) in different regions, i.e., USA, Mexico, and Canada, that can direct you in mapping the regional demand.

8. Demand by Sales Channel (Direct and Indirect)

Multiple channels are used to sell Poly Vinyl Chloride (PVC). Our sales channel will help in analyzing whether distributors and dealers or direct sales make up most of the industry's sales.

9. Demand-Supply Gap

Determine the supply-demand gap to gain information about the trade surplus or deficiency of Poly Vinyl Chloride (PVC).

10. Company Share

Figure out what proportion of the market share of Poly Vinyl Chloride (PVC) is currently held by leading players across the globe.

11. Country-wise Export

Get details about quantity of Poly Vinyl Chloride (PVC) exported by major countries.

12. Country-wise Import

Get details about quantity of Poly Vinyl Chloride (PVC) imported by major countries.

13. Manufacturing Process

Discover insights into the intricate manufacturing process of Poly Vinyl Chloride (PVC).

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

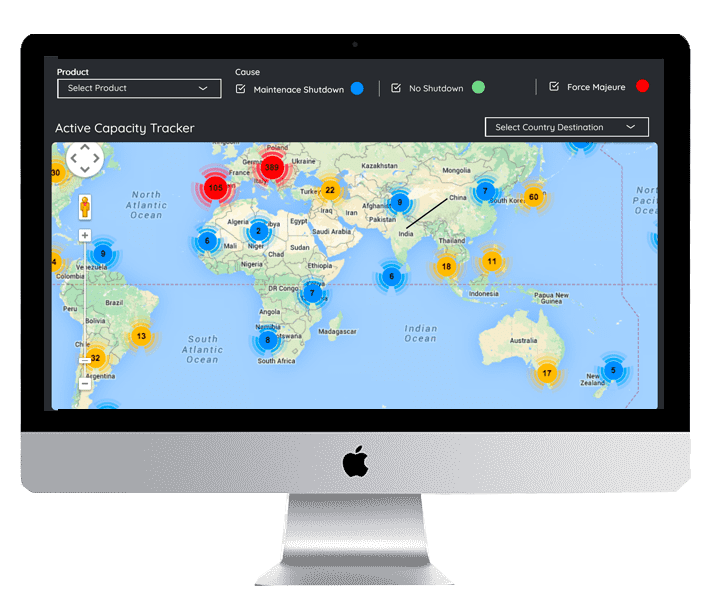

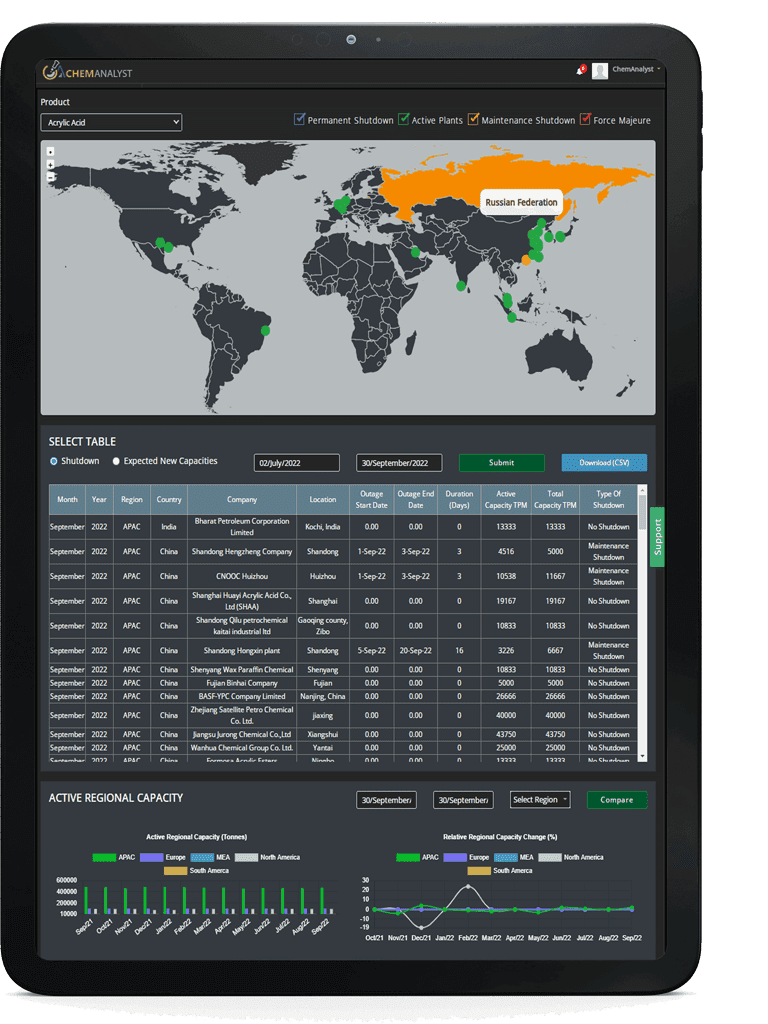

Disruption Tracker

Disruption Tracker reflect the major shutdown on monthly basis which will help you in

tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions

resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries

with a global view of production and consumption capacity loss that reflects the corresponding conversion factors.

It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up

of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case

of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight

into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on

supply of the product in the market at a Global level.

The size of North America Poly Vinyl Chloride (PVC) market has grown significantly in the historic period and reached approximately 7.5 million tonnes in 2023.

Online Access 12 Months – Single User License (Up to 3 users can access the database) Online Access 12 Months – Enterprise License (Up to 10 Users can access the database)

You will have 24/7 access to the analyst during the subscription period.

Our Solutions

Custom Research

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

Techno Economic Feasibility Report (TEFR)

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Price Benchmarking

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.

We use cookies to deliver the best possible experience on our website. To learn more, visit our

Privacy Policy.

By continuing to use this site or by closing this box, you consent to our use of cookies.

More info.