H1 2023: In June 2023, QatarEnergy signed definitive agreements with China National Petroleum Corporation (CNPC). The companies signed binding agreements for the long-term supply of liquefied natural gas (LNG) to China and collaboration in the North Field East LNG expansion project (NFE). A 27-year long-term LNG Sales and Purchase Agreement (SPA) has been inked between CNPC and Qatar. According to the agreement, 4 million tonnes of liquefied natural gas would be delivered annually from the NFE project to the receiving terminals of CNPC in China. In June 2023, Equinor and Cheniere agreed to a 15-year Sales and Purchase Agreement (SPA) for the purchase of about 1.75 million tonnes of LNG annually. Half of the supply is expected to start in 2027. With the addition of this new agreement, Equinor's committed volumes with Cheniere now amount to about 3.5 million tonnes annually. By the agreement, Equinor's planned LNG exports from Cheniere's LNG terminals along the Gulf of Mexico will practically quadruple. In the same month of June, a collaboration contract was inked by NOVATEK to carry out a small-scale LNG investment project in the Tula Region. The agreement calls for the development of a small-scale LNG facility in the Tula Region on land belonging to the "Uzlovaya" special economic zone. The plant will have an annual production capacity of 126 thousand tonnes. This LNG facility in the Central Federal District of the Russian Federation will provide LNG as both an off-grid energy source and as vehicle fuel through an LNG fueling network.

The global liquefied natural gas (LNG) market is expected to experience substantial growth in the coming years due to the increasing demand for electric power from clean energy sources. This growth will be further supported by a rising focus on distributed power and utility projects over the next few years. As natural gas becomes more prevalent in the power generation sector, the demand for LNG is also expected to rise in various countries.

LNG is natural gas that has been cooled to a liquid state for ease of storage and transportation, enabling its movement across long distances and to regions without access to natural gas pipelines. Coal remains a dominant source of electricity generation globally, but due to concerns about depleting coal reserves and its environmental impact, there has been a noticeable shift toward using natural gas and other renewable energy sources for electricity production. The market plays a vital role in meeting the world's increasing demand for cleaner and more sustainable energy sources.

Market Drivers

Rising Demand for LNG as Cleaner Fuel for Electricity Generation

The global demand for electricity from clean energy sources has witnessed a remarkable surge, propelling the liquefied natural gas (LNG) market to new heights. As concerns over greenhouse gas emissions and environmental impact intensify, governments and industries worldwide are seeking cleaner alternatives to traditional fossil fuels like coal. LNG has emerged as a viable solution, offering a cleaner burning fuel option for electricity generation. With its lower carbon footprint compared to coal and other hydrocarbon-based fuels, LNG has become a significant player in the transition towards more sustainable energy sources. The shift towards LNG in electricity generation is expected to have far-reaching implications on the global energy landscape, fostering a greener and more environmentally responsible future.

Expanding LNG Market Through Distributed Power and Utility Projects

A key factor driving the expansion of the global LNG market is the growing emphasis on distributed power and utility projects. These initiatives involve generating power from smaller-scale sources that are situated closer to the end-users, decentralizing the energy production process. Distributed power systems benefit from the flexibility and efficiency of LNG as a fuel choice, making it an attractive option for powering remote areas and regions lacking access to traditional power grids. The inherent advantages of LNG, such as ease of storage and transportation, enable efficient delivery to these decentralized energy systems. As governments and organizations prioritize sustainability and energy security, the rising interest in distributed power and utility projects is set to boost the demand for LNG, opening up new opportunities for market growth and innovation in the energy sector.

Furthermore, the increased adoption of natural gas in the power generation business is contributing to the surge in LNG demand worldwide. Governments and industries are embracing natural gas as a transitional fuel, given its lower carbon emissions compared to coal, oil, or other hydrocarbon-based energy sources.

Market Restraints

Capital-Intensive Infrastructure Development

One of the significant challenges facing the global LNG market is the capital-intensive nature of infrastructure development. Establishing liquefaction terminals and regasification facilities requires substantial investments due to the sophisticated technology and engineering involved. These facilities are crucial for the liquefaction of natural gas into LNG and the subsequent regasification process before distribution and consumption. The financial burden of setting up these facilities can pose obstacles for new market entrants and countries seeking to expand their LNG capabilities. Moreover, the long lead times associated with constructing such infrastructure can impact supply chain timelines and the ability to respond quickly to changing market dynamics.

Geopolitical Factors and Trade Dynamics

Geopolitical factors and international trade dynamics present another set of challenges for the global LNG market. As LNG is traded across international borders, geopolitical tensions can lead to disruptions in supply chains and impact market prices. Political conflicts or trade disputes between exporting and importing countries can lead to restrictions or tariffs, influencing the flow of LNG to specific regions. Uncertain regulatory environments in some countries can also affect the stability of long-term contracts and investment decisions in the LNG sector. Additionally, changing trade policies and agreements can create uncertainties, making it difficult for industry players to plan for the future with confidence. Navigating these geopolitical complexities requires strategic foresight and risk management to mitigate potential disruptions to the global LNG market.

Trends & Opportunities

Growing Adoption of Floating LNG (FLNG) Facilities

The global LNG market is witnessing a significant trend with the increasing adoption of Floating LNG (FLNG) facilities. These innovative offshore floating vessels enable LNG production directly at offshore gas fields, eliminating the need for costly onshore infrastructure and reducing environmental impacts. FLNG offers various advantages, including improved access to remote offshore gas reserves, enhanced efficiency, reduced transportation costs, and faster deployment compared to traditional onshore LNG plants. Additionally, FLNG facilities adhere to advanced environmental and safety standards, contributing to reduced greenhouse gas emissions and minimizing the impact on coastal ecosystems. As the demand for LNG rises and offshore gas reserves become more critical, the adoption of FLNG technology is expected to grow, transforming the dynamics of the global LNG market, and expanding LNG production to previously untapped areas.

The future of the global LNG market appears promising, with a projected compound annual growth rate (CAGR) of 5.12% expected over the next decade. As the world continues to prioritize reducing carbon emissions and transitioning to cleaner energy sources, LNG is positioned to play a pivotal role in the global energy mix. Technological advancements in LNG infrastructure, evolving trade agreements, and ongoing efforts to decarbonize the energy sector are likely to shape the market's growth trajectory in the years to come.

End-Use Analysis

Power generation, industrial use, residential and commercial sectors, and others are the key end users of liquefied natural gas across the world. Among these, the power generation segment led the global market with a value of around US$ 63,100 Million in 2022. The segment is expected to continue its dominance over the forecast period due to the increasing focus on sustainable clean energy sources.

The second leading end user in this market is the industrial use segment, which is projected to retain its position over the next few years. The industrial use of LNG is expected to grow as industries continue to prioritize sustainability and seek more environmentally friendly energy sources to power their operations. As a versatile and cleaner fuel option, LNG provides a viable solution for meeting industrial energy needs while reducing carbon footprints.

Regional Analysis

The LNG market reports its presence across North America, Europe, Asia Pacific, South America, and the Middle East and Africa. Asia Pacific has surfaced as the largest and most dominant market for LNG across the world. China's rapid economic growth has led to a surge in LNG imports to meet its increasing energy needs and reduce air pollution from coal. India's rising energy demand and focus on cleaner energy sources have also boosted LNG imports significantly. The region's LNG market is witnessing infrastructure expansion in many economies, enhancing supply capabilities, which is likely to support the regional market over the forthcoming years.

Among other regions, North America has a prominent presence in the global LNG market. With the United States being a significant player in the LNG market due to its shale gas boom, the region is expected to remain demonstrating healthy growth over the forecast period.

Competitive Landscape

ExxonMobil, Eni, Royal Dutch Shell, Chevron Corporation, Qatar Petroleum (QP), TotalEnergies, Petronas, BP, Novatek, and Woodside Energy are some of the key players in the global LNG market. The market is highly competitive, characterized by a diverse range of companies from various regions actively engaged in LNG production, liquefaction, transportation, and trading. Key players in the market compete based on several factors, such as production capacity, market presence, technological advancements, supply chain efficiency, and customer relationships.

The competitiveness in the market is shaped by a combination of production capacity, technological advancements, market access, and environmental considerations. As the world's energy landscape evolves, companies are adapting to changing market conditions, meeting sustainability goals, and providing reliable LNG supply to thrive in the competitive global LNG market.

Years considered for this report:

Historical Period: 2015-2022

Base Year: 2022

Estimated Year: 2023

Forecast Period: 2024-2032

This report will be delivered on an online digital platform with one-year subscription and quarterly update.

The objective of the Study:

• To assess the demand-supply scenario of LNG, which covers the production, demand, and supply of the LNG market.

• To analyze and forecast the size of the LNG market.

• To classify and forecast the LNG market based on end-use and regional distribution.

• To examine competitive developments, such as expansions, mergers & acquisitions, and partnerships, of the LNG market.

To extract data for the LNG market, primary research surveys were conducted with LNG manufacturers, suppliers, distributors, wholesalers, and traders. While interviewing, the respondents were also inquired about their competitors. Through this technique, ChemAnalyst was able to include manufacturers that could not be identified due to the limitations of secondary research. Moreover, ChemAnalyst analyzed various segments and projected a positive outlook for the LNG market over the coming years.

ChemAnalyst calculated the demand for LNG in the world by analyzing the historical data and demand forecast which was carried out considering the demand for LNG by end users across the world. ChemAnalyst sourced these values from industry experts, and company representatives and externally validated them by analyzing the historical sales data of respective manufacturers to arrive at the overall market size. Various secondary sources such as company websites, association reports, annual reports, etc., were also studied by ChemAnalyst.

Key Target Audience:

• LNG manufacturers and other stakeholders

• Organizations, forums, and alliances related to LNG distribution

• Government bodies, such as regulating authorities and policymakers

• Market research organizations and consulting companies

The study is useful in providing answers to several critical questions that are important for industry stakeholders, such as LNG manufacturers, customers, and policymakers. The study would also help them to target the growing segments over the coming years (next two to five years), thereby aiding the stakeholders in taking investment decisions and facilitating their expansion.

Report Scope:

In this report, the LNG market has been segmented into the following categories, in addition to the industry trends, which have also been detailed below:

Attribute

Details

Market Size Volume in 2022

21,222 MMBtu

Market Size Volume by 2032

33,330 MMBtu

Growth Rate

CAGR of 5.12% from 2023 to 2032

Base Year for Estimation

2023

Historical Data

2015 - 2022

Forecast Period

2024 - 2032

Quantitative Units

Demand in MMBtu and CAGR from 2023 to 2032

Report Coverage

Industry Market Size, Demand by End-Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Foreign Trade, Manufacturing Process, and Policy and Regulatory Landscape.

Segments Covered

By End-Use: Power Generation, Industrial Use, Residential and Commercial Sectors, and Others

By Sales Channel: Direct Sales and Indirect Sales

Regional Scope

North America, Europe, Asia Pacific, the Middle East and Africa, and South America.

With the given market data, ChemAnalyst offers customizations according to a company’s specific needs.

In case you do not find what you are looking for, feel free to connect with our custom research team at sales@chemanalyst.com

Market Data & Insights

Table of Content

1. Industry Market Size

It is an essential metric for market analysis, as it provides insights into the overall size and growth potential of the LNG market in terms of value and volume.

2. Demand by End-Use [Quarterly Update]

Discover which end-user industries (Power Generation, Industrial Use, Residential and Commercial Sectors, and Others) are creating a market and the forecast for the growth of the LNG market.

3. Demand by Region

Analyzing the change in demand for LNG in different regions, i.e., North America, Europe, Asia Pacific, the Middle East and Africa, and South America, can direct you in mapping the regional demand.

4. Demand by Sales Channel (Direct and Indirect)

Multiple channels are used to sell LNG. Our sales channel will help in analyzing whether distributors and dealers or direct sales make up most of the industry's sales.

5. Demand-Supply Gap

Determine the supply-demand gap to gain information about the trade surplus or deficiency of LNG.

6. Country-wise Export

Get details about the quantity of LNG exported by major countries.

7. Country-wise Import

Get details about the quantity of LNG imported by major countries.

8. Manufacturing Process

Discover insights into the intricate manufacturing process of LNG.

9. Policy and Regulatory Landscape

Gain a comprehensive understanding of the policy and regulatory landscape within the LNG market.

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

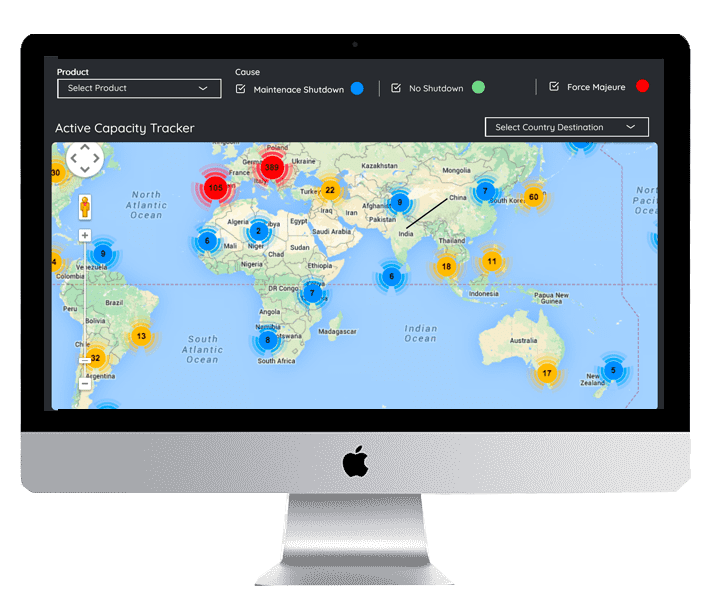

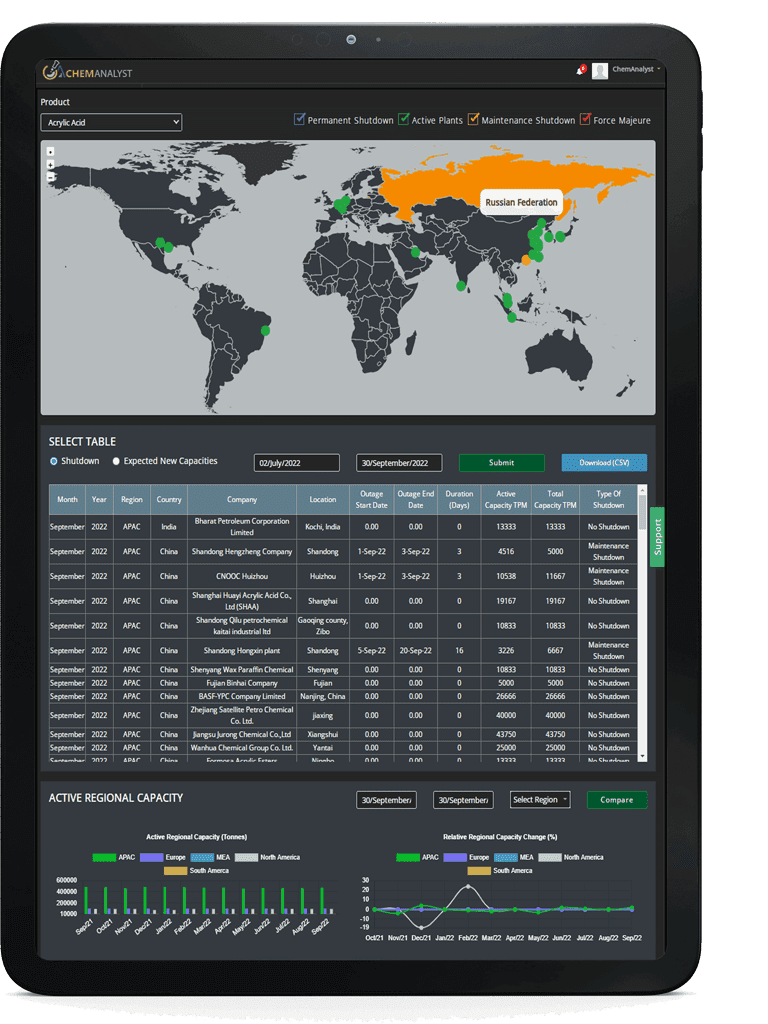

Disruption Tracker

Disruption Tracker reflect the major shutdown on monthly basis which will help you in

tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions

resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries

with a global view of production and consumption capacity loss that reflects the corresponding conversion factors.

It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up

of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case

of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight

into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on

supply of the product in the market at a Global level.

What are the key factors driving the global LNG market?

Ans:

The increasing demand for electricity from clean energy sources is boosting the global LNG market. This growth will be further supported by a rising focus on distributed power and utility projects over the next few years.

Q2.

Which is the leading end-use segment in the global LNG market?

Ans:

Power Generation sector is the dominant end-use segment in the global LNG market.

Q3.

Which region is likely to lead the global LNG market during the forecast period?

Ans:

Asia Pacific is likely to lead the global LNG market during the forecast period.

Q4.

Do you offer single or multiuser license?

Ans:

Online Access 12 Months – Single User License (Up to 3 users can access the database) Online Access 12 Months – Enterprise License (Up to 10 Users can access the database)

Our Solutions

Custom Research

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

Techno Economic Feasibility Report (TEFR)

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Price Benchmarking

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.

We use cookies to deliver the best possible experience on our website. To learn more, visit our

Privacy Policy.

By continuing to use this site or by closing this box, you consent to our use of cookies.

More info.